Introduction

Student life is exciting because it offers new experiences, friendships, and opportunities to learn. However, it also brings financial responsibilities that many young people have never faced before. Whether you receive money from your family, earn through a part-time job, or depend on scholarships, learning how to manage your finances is an essential life skill. Without a proper plan, it is easy to overspend and struggle before the end of the month.

That is why understanding budgeting tips for students is so important. A budget is not about restricting yourself from enjoying life. Instead, it helps you make smarter decisions with the money you have. By tracking income and expenses, you can spend confidently, avoid unnecessary debt, and save for future goals.

Many students believe budgeting is difficult or only necessary for adults. In reality, the earlier you learn this skill, the easier it becomes to build healthy financial habits. Even a simple budget can help reduce stress, improve financial confidence, and prepare you for life after graduation.

In this guide, you will discover practical budgeting tips for students, learn why budgeting matters, and explore step-by-step methods to create a budget that works. Whether you are living at home, staying in a hostel, or renting an apartment, these strategies will help you stay in control of your finances.

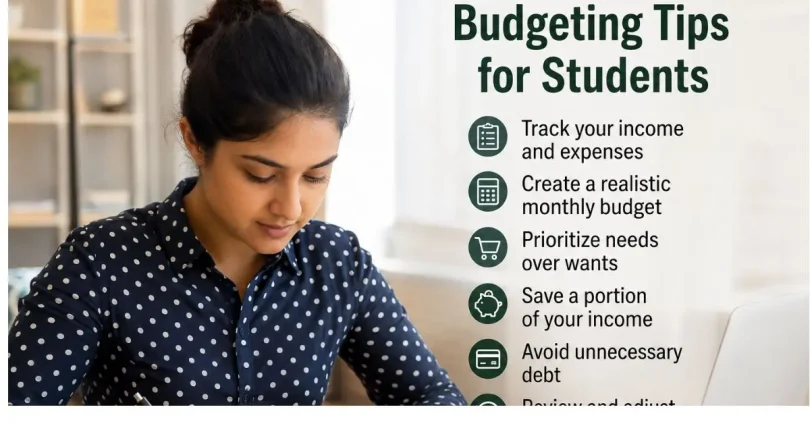

What Are Budgeting Tips for Students?

Budgeting tips for students are practical strategies that help students manage their money wisely. These tips focus on planning income, controlling expenses, saving regularly, and making informed financial decisions. Instead of spending money without a plan, students learn how to allocate funds for necessities while still leaving room for entertainment and personal goals.

A student budget usually includes:

- Monthly income

- Tuition or education expenses

- Books and study materials

- Food and groceries

- Transportation

- Mobile and internet bills

- Entertainment

- Savings

- Emergency expenses

For example, imagine a student receives $300 every month. Without a budget, the money may disappear within two weeks because of unnecessary spending. However, by assigning specific amounts to different categories, the same student can cover essential expenses, save a small amount, and still enjoy social activities.

Budgeting is not about having a large income. It is about making the best use of whatever money you have. Even students with limited funds can benefit greatly from proper financial planning.

Why Are Budgeting Tips for Students Important?

Learning to manage money during student life provides benefits that extend well into adulthood. Financial habits developed today often shape future financial success.

One major reason budgeting matters is that it prevents overspending. When students know exactly how much money they have available, they become more careful about unnecessary purchases. This reduces the chances of running out of money before the month ends.

Budgeting also lowers financial stress. Worrying about unpaid bills or lacking money for essential needs can affect academic performance. A clear spending plan provides peace of mind because students know their finances are under control.

Another important benefit is that budgeting encourages saving. Even setting aside a small amount every month creates an emergency fund that can help during unexpected situations such as medical expenses or urgent travel.

Furthermore, budgeting teaches responsibility. Students become more aware of their financial choices, making them better prepared for independent living after graduation.

Finally, budgeting helps students achieve personal goals. Whether saving for a new laptop, paying course fees, or planning a trip, a good financial plan makes these goals more realistic and achievable.

Step-by-Step Guide to Budgeting Tips for Students

Step 1: Know Your Monthly Income

The first step in creating a budget is identifying every source of income. Many students underestimate how much money they actually receive because they forget occasional earnings.

Your income may include:

- Family allowance

- Part-time job salary

- Scholarships

- Freelance income

- Internship payments

- Small business earnings

- Gifts or occasional financial support

Write down your average monthly income. If your earnings change each month, use the lowest expected amount when planning your budget. This prevents overspending.

For example:

Monthly family support: $200

Part-time job: $180

Freelance work: $70

Total monthly income: $450

Knowing this number gives you a realistic starting point.

Step 2: Track Every Expense

Many students are surprised when they discover where their money actually goes. Small daily purchases often add up faster than expected.

For one month, record every expense without exception. Include even inexpensive items like snacks, coffee, or online subscriptions.

Common student expenses include:

- Rent

- Groceries

- Transportation

- School supplies

- Internet

- Phone bills

- Streaming services

- Dining out

- Entertainment

- Clothing

- Personal care products

After tracking your spending, group expenses into categories. This makes it easier to identify areas where you can reduce unnecessary costs.

For instance, spending a few dollars every day on drinks or fast food may seem harmless, but over a month it can become one of your largest expenses.

Step 3: Separate Needs from Wants

One of the smartest budgeting habits is learning the difference between needs and wants.

Needs are essential expenses that you must pay to live and study comfortably. Wants are optional purchases that improve enjoyment but are not necessary.

Examples of needs include:

- Tuition fees

- Rent

- Groceries

- Transportation

- Study materials

- Utility bills

Examples of wants include:

- Expensive coffee

- Gaming purchases

- Designer clothing

- Frequent restaurant meals

- Entertainment subscriptions

- Impulse online shopping

This does not mean you should eliminate all wants. Instead, prioritize needs first and enjoy wants within your remaining budget.

When money becomes limited, cutting optional expenses is much easier than reducing essential ones.

Step 4: Create Spending Categories

Now that you know your income and expenses, divide your money into clear categories.

A simple example might look like this:

- Housing

- Food

- Transportation

- Education

- Savings

- Entertainment

- Emergency fund

- Miscellaneous expenses

Assign a realistic amount to each category based on your priorities.

The goal is to ensure every dollar has a purpose before you spend it. This approach reduces impulsive purchases and keeps your finances organized.

Step 5: Set Realistic Savings Goals

Many students think saving is only possible when they have a large income. In reality, even saving a small amount consistently can make a significant difference over time. The habit of saving is often more important than the amount itself.

Start by deciding what you want to save for. Your goal could be buying a new laptop, paying for future tuition, covering emergency expenses, or taking a short vacation after exams. Having a clear purpose makes it easier to stay motivated.

You can also use the “pay yourself first” approach. As soon as you receive your monthly income, move a fixed amount into your savings before spending on anything else. Even saving five or ten percent of your income can build a helpful financial cushion over time.

Step 6: Use Budgeting Apps or Simple Spreadsheets

Managing your budget becomes much easier when you keep accurate records. Fortunately, you do not need complicated software. A notebook, spreadsheet, or budgeting app can all work effectively.

Choose a system that you will actually use consistently. Record your income, update your expenses, and review your remaining balance regularly.

A weekly review only takes a few minutes, but it helps you spot problems before they become serious. If one category is exceeding your budget, you can make adjustments before the month ends.

Step 7: Reduce Unnecessary Expenses

Saving money does not always require earning more. Sometimes it simply means spending more wisely.

Look for expenses that provide little value. For example, buying coffee every morning, ordering food several times each week, or subscribing to services you rarely use can quietly consume a large portion of your monthly budget.

Consider these practical ways to reduce costs:

- Prepare meals at home whenever possible.

- Borrow or purchase used textbooks.

- Use student discounts.

- Share accommodation or transportation costs.

- Cancel subscriptions you no longer need.

- Compare prices before making purchases.

Small changes repeated every month often produce impressive long-term savings.

Step 8: Build an Emergency Fund

Unexpected expenses can happen at any time. A medical emergency, damaged laptop, urgent travel, or sudden repair can quickly disrupt your finances.

An emergency fund provides protection during these situations. Instead of borrowing money or using credit, you can rely on your savings.

Aim to save enough to cover at least one month of essential expenses. If that feels difficult, begin with a smaller target and increase it gradually.

Step 9: Review Your Budget Every Month

A budget should never remain exactly the same forever. Your income, expenses, and priorities may change throughout the year.

Review your budget at the end of each month by asking yourself:

- Did I stay within my spending limits?

- Which expenses were higher than expected?

- Where did I save money?

- What should I improve next month?

Regular reviews help you learn from experience and create a budget that becomes more accurate over time.

Benefits of Budgeting Tips for Students

Following a budget offers many advantages beyond simply saving money.

- Helps control unnecessary spending.

- Reduces financial stress.

- Encourages regular saving habits.

- Improves financial confidence.

- Helps prepare for unexpected emergencies.

- Makes it easier to achieve financial goals.

- Reduces dependence on loans or borrowing.

- Encourages responsible decision-making.

- Supports better academic focus by reducing money worries.

- Builds lifelong money management skills.

- Creates discipline and self-control.

- Makes future financial planning easier.

Students who budget consistently often feel more confident because they understand exactly where their money goes each month.

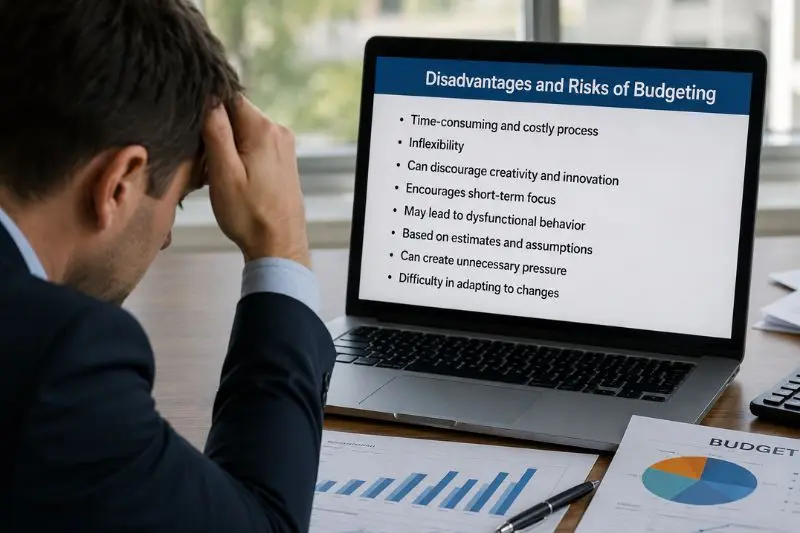

Disadvantages and Risks of Budgeting

Although budgeting is highly beneficial, there are a few challenges to consider.

- Creating a budget requires discipline and consistency.

- Tracking every expense can feel time-consuming at first.

- Unexpected emergencies may temporarily disrupt your financial plan.

- Overly strict budgets can become difficult to maintain.

- Income fluctuations may require frequent adjustments.

- Ignoring your budget for long periods reduces its effectiveness.

Fortunately, these challenges become much easier to manage as budgeting becomes a regular habit.

Common Mistakes to Avoid

Many students make simple budgeting mistakes that can easily be prevented.

One common mistake is forgetting to track small daily expenses. A snack, drink, or online purchase may seem insignificant, but together they can consume a surprising amount of money.

Another mistake is creating unrealistic budgets. If your budget completely removes entertainment or social activities, you may struggle to follow it consistently. A balanced plan is usually more successful.

Some students also fail to review their budgets regularly. Financial situations change, so your budget should change as well.

Ignoring savings is another common problem. Waiting until the end of the month to save often results in having nothing left. Saving first is usually much more effective.

Finally, avoid impulse buying. Give yourself time before making non-essential purchases. Waiting even twenty-four hours can help you decide whether you truly need the item.

FAQs

Why should students create a budget?

A budget helps students control spending, reduce financial stress, save money, and prepare for future expenses. It also teaches valuable money management skills that remain useful throughout life.

How much should a student save each month?

The amount depends on individual income and expenses. Even saving five to ten percent of monthly income is a great starting point. Consistency matters more than saving large amounts.

What is the easiest budgeting method for beginners?

A simple monthly budget that lists income, essential expenses, savings, and optional spending is usually the easiest approach. Tracking expenses consistently is more important than using a complicated system.

Should students use cash or digital payments?

Both options can work well. Cash makes it easier to see how much you are spending, while digital payments provide convenience and automatic records. Choose the method that helps you stay within your budget, or combine both for better control.

How often should a student review a budget?

Reviewing your budget once every week helps you monitor spending and make quick adjustments. A detailed monthly review is also important because it allows you to evaluate your financial progress and improve your budget for the following month.

Can budgeting help reduce debt?

Yes. A well-planned budget helps you spend within your means, avoid unnecessary borrowing, and repay existing debt more efficiently. It also encourages saving, which reduces the need to rely on loans during emergencies.

Expert Tips & Bonus Points

Learning to budget is a journey rather than a one-time task. The following expert tips can help you build stronger financial habits and achieve better results.

- Set clear financial goals for both the short and long term.

- Save first before spending on non-essential items.

- Keep a small emergency fund for unexpected situations.

- Compare prices before making large purchases.

- Take advantage of student discounts whenever available.

- Prepare meals at home to reduce food expenses.

- Avoid shopping when you are bored or stressed.

- Review your subscriptions every few months and cancel those you no longer use.

- Track your progress and celebrate small financial achievements.

- Stay patient and consistent because successful budgeting is built through regular habits rather than overnight changes.

Remember that every student’s financial situation is different. Focus on creating a budget that fits your income, lifestyle, and goals instead of comparing yourself with others.

Conclusion

Managing money wisely is one of the most valuable skills a student can develop. While earning a large income may not be possible during your academic years, learning how to use the money you already have effectively can make a significant difference. By following practical budgeting tips for students, you can stay in control of your finances, avoid unnecessary stress, and create a solid foundation for future financial success.

A successful budget starts with understanding your income, tracking your expenses, separating essential needs from optional wants, and setting realistic savings goals. These simple habits help you make informed financial decisions instead of spending impulsively. Over time, even small improvements in your spending habits can lead to meaningful savings and greater financial confidence.

Remember that budgeting is not about giving up everything you enjoy. Instead, it is about spending intentionally and ensuring your money supports your priorities. Whether your goal is paying tuition fees, buying study materials, building an emergency fund, or saving for a personal achievement, a well-planned budget helps you reach those milestones more efficiently.

It is also important to review your budget regularly. Your income, expenses, and personal goals may change throughout the year, so your financial plan should evolve as well. By monitoring your progress each month, you can identify areas for improvement, adjust your spending, and continue building healthy financial habits.

The lessons you learn from budgeting as a student will continue to benefit you long after graduation. Strong money management skills can help you reduce debt, prepare for unexpected expenses, achieve long-term financial goals, and enjoy greater peace of mind throughout your life. Employers, business owners, and financially successful individuals all understand the importance of planning, discipline, and responsible decision-making, and budgeting helps you develop these qualities early.

Most importantly, do not be discouraged if your first budget is not perfect. Every month is an opportunity to learn, improve, and become more confident in managing your finances. Stay consistent, remain patient, and focus on steady progress rather than perfection. Every smart financial decision, no matter how small, brings you closer to financial independence, greater security, and a brighter future. By applying these budgeting tips consistently, you can build lifelong financial confidence and enjoy the benefits of responsible money management for years to come.